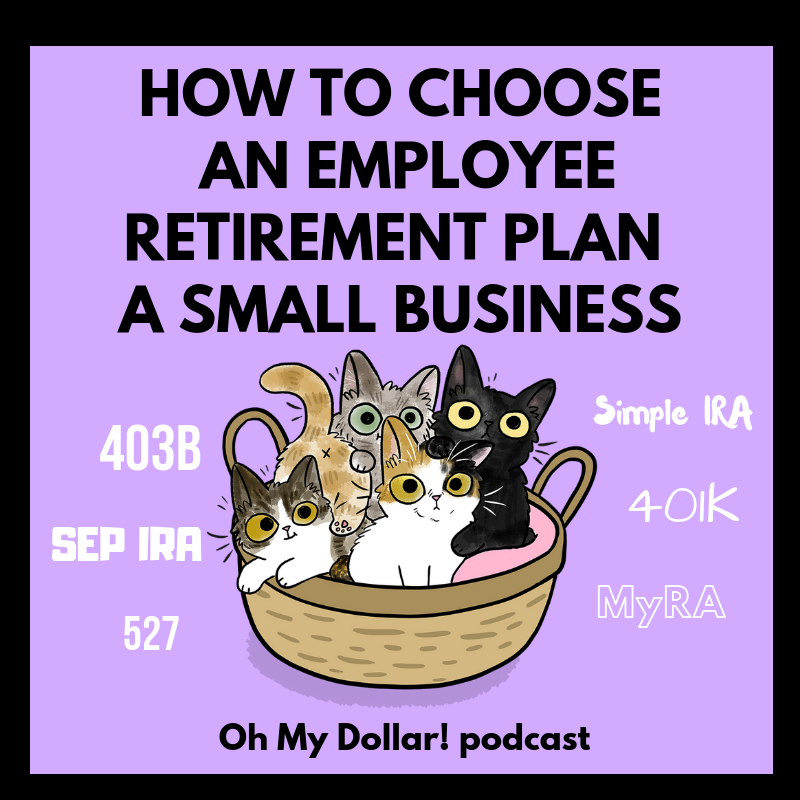

There’s so many options out there for small business retirement plans for employers! How do you choose one you can afford and that won’t cause headaches to administer?

Marcel wrote in: I’m a small business owner, who has recently expanded to have 8 employees. We’re doing well as a business, and I’d like to encourage my employees to save for retirement. What are my options?

Almost all these plans will require you to make any eligible employee able to use it, which means you can’t set up one just for yourself as the business owner without also providing something to your eligible employees. You have the ability to set eligibility standards, but all accounts have a minimum requirement for employee eligibility (such as if they’ve worked there for 1000 hours a year, for at least a year, they have to have access to the account.) This is important to bare in mind if you are making employer contributions but have part-time or seasonal employees.

Your options as an employer

– Simple IRA: A relatively simple to administer retirement account that requires employer contributions of at least 2% of the employee’s salary, even if the employees don’t contribute anything. There are no IRS filing requirements for the employer but you can only offer this plan. The annual contribution limit is $13,000 for employees under 50.

– SEP: A SEP (Simplified Employee Pension) IRA A traditional IRA for self-employed people or small business owners. It has more recordkeeping requirements A small business owner with one employee or more, or anyone with a freelance income can open a SEP IRA. These are advantageous for owners because the contribution limits are high, but no employees can contribute to this plan for themselves – it’s just employer contributions. Individual employees who are eligible to participate in their employer’s SEP plan must open individual Traditional IRAs to which their employers will deposit SEP contributions.

-401k/403B This is the “traditional” retirement plan, and it has the headaches meant for a large employer to administer it as far as recordkeeping requirements. It has the highest limits for non-owner employees, $18.500 per year for employees under 50.

–Allowing employees to contribute to a Roth or Traditional IRA through automatic deduction This has no cost to you, just a little more work during payroll. Unless the Traditional IRA is set up as a SEP, you cannot contribute as an employer to these plans.

-[No Longer Available] MyRA: A beginner retirement account for your employees that is a government-bond backed IRA, now closed under the current administration.

Links Mentioned

– OregonSaves, Oregon’s automatic retirement plan that is a government-administered Roth IRA. This is now compulsory for any Oregon employer that has no other retirement plan in place for employees.

Please come join us

We finally have a forum! Join us at forum.ohmydollar.com is a great non-judgemental place to ask questions or participate in our daily check-ins and challenges. It’s really quite fun. Most of the forum is hidden from view, so register to see more!

Ask us a question!

We love hearing from you! Email us your questions or successes at questions@ohmydollar.com or tweet us at @anomalily or @ohmydollar

This show is made paw-sible by listeners like you

We absolutely love our Purrsonal Finance Society Members, the folks that generously support Oh My Dollar with $1 or more a month on Patreon – and have made is so we have free, full transcripts for every show on ohmydollar.com. This episode was underwritten by patron Tamsen G Association and Warrior Queen. To learn more about being part of the Purrsonal Finance Society and get cool perks like exclusive livestreams and cat stickers, you can visit ohmydollar.com/support

Other Episodes You Might Find interesting

- Oregon is making retirement plans a requirement for everyone ft. Joel Metlan – The OregonSaves plan for employers

- The Government Will Pay You to Save For Retirement – the saver’s credit, a great way to sell lower-income-earning employees on retirement savings

- New Year’s Resolution: Pay Less Taxes . – all about tax planning with a SEP for self-employed folks

Full Transcript provided by our Patrons

How to Choose An Employee Retirement Plan as a Small Business (transcribed by Sonix)

Will Romey: This show was supported by generous listeners like you. You’re a patriot.

Will Romey: This episode was underwritten by the Tamsen G Association and Chris Giddings. To learn more about cool ways to support Oh My Dollar! and get perks like exclusive livestream and cat stickers you can visit, ohmydollar.com/support

Lillian Karabaic: Welcome to Oh My Dollar!, a personal finance show with a dash of glitter. Dealing with money can be scary and stressful. Here, we give practical, friendly advice about money that helps you tackle the financial overwhelm. I’m your host, Lillian Karabaic.

Will Romey: I’m your other host, Will.

Lillian Karabaic: We have a listener question today. And honestly there’s a lot to tackle here – so, I think that’s the whole episode. Will do you want to read what Marcel wrote? Yes.

Will Romey: Marcel wrote in “I’m a small business owner and I’ve recently expanded to have eight employees. We’re doing well as a business and I’d love to encourage my employees to save for retirement. What are my options as an employer?”

Lillian Karabaic: Marcel, this is great because we’ve talked before about what you can do if you’re self-employed or if you have the employer-based options, but if you are an employer yourself, how do you set things up?

Lillian Karabaic: So, there’s a couple different options and there’s different kinds of buckets to think about.

Lillian Karabaic: So, there are buckets that are purely based on you contributing as an employer so they are you know just essentially contributing as an employer. And what the employee does has nothing to do with it.

Lillian Karabaic: There are options that require you to offer a match as an employer which means that you’ll put up some of your own money into the employees IRA.

Will Romey: Yeah.

Lillian Karabaic: And then there’s some other options which are essentially just like an IRA, that you are establishing as an option for employees and you will do the automatic deductions out, but it’s just like they would have an IRA outside of work.

Will Romey: Oh! You wouldn’t be matching per see you’d just be sort of setting up that infrastructure.

Lillian Karabaic: Yeah and then kind of the last option are the more traditional options that you think up with large employers like 401K, 403Bs, 457s, and those are the thing that I will probably most likely warn you away from as an employer.

Lillian Karabaic: And the reason I would warn you away from something like a 401K or a 403B – is these are – which, you know we’ve talked about before. Those are essentially types of accounts that allow you to save for retirement. The current year’s limit is $19,000 per employee and you have the option of matching or not matching as an employer.

Lillian Karabaic: Here’s the thing about for one case – as a small business that only has eight employees, 401K’s cost you a bunch of time an administration, you need to have, you you are responsible as the employer for keeping on top of rules and regulations as they change. And even though you’ll use a third party vendor, a brokerage which would be something like Vanguard or Fidelity or one of those companies. You still have to follow all of these rules, and these rules and documents that you need to file and everything can can be kind of a pain in your butt but you really don’t – you want to worry about your business, right?

Lillian Karabaic: You’re not in the business of being a 401K provider, you just want to treat your employees well, and make sure that they’re saving for their future. And frankly, 401Ks, are a lot of work. And so unless you have someone who has plan administration as a large part of their job I wouldn’t recommend it.

Will Romey: And then that’s why it makes more sense for like a larger business with larger overhead to have that sort of thing.

Lillian Karabaic: Yeah and and a lot of the options I’m about to talk about will not apply to you, if you have more than like 100 employees, and so that’s important to understand is a lot of the things I’m talking about are specific to smaller employers. Almost all of the ones I’m going to talk about only apply to for-profit businesses.

Lillian Karabaic: There are a couple of these that you can do if you are a non-profit and you’re looking to set up retirement plans for your employees. So I will note as we go through them. So, the first option is kind of those those 401KS – and they do take a lot of work. You have to do what’s called “means testing” which is making sure that you’re you know not giving too many of the higher compensated employees more access to the 401K, you you have to set up this plan administration.

Lillian Karabaic: It’s a lot of work it is a thing that you can do but.

Will Romey: And there’s full time people who like administrate these things in many cases, Right?

Lillian Karabaic: Right. Right. Yeah definitely. And I’ve worked at non-profits that have had them and not had a plan administrator that knows what they’re doing – and it’s a bunch of work to dig up those documents and make sure they’re updated when the law is changed.

Lillian Karabaic: But, if you are a small business that is only self-employed you can do what’s called is Solo 401K and a Solo Roth 401K and this only works if you don’t have any other employees. So Marcel would not be in the category of this, but those are a lot easier to administer because obviously you don’t have to do really any testing.

Will Romey: A yaya that makes sense.

Lillian Karabaic: And those can be really great, if you’re trying to reduce your taxable income because those- the solo 401K is going to be pre-tax and you can contribute both on the employer and the employee side. So it can be up to fifty six thousand dollars depending on how much earned income.

Will Romey: Now this is maybe a stupid question but would putting – would matching employee contributions to these accounts reduce the employer’s taxable income?

Lillian Karabaic: Yes it would. And so doing matching generally is, its business overhead right? And so this is a it’s a business expense. Some of the things that changed in the new tax law do affect generally how this is.

Lillian Karabaic: But this is tax deductible just the same as like when you pay an employee as an employer that you’re you know you are paying part of their taxes. But like the amount that you pay them is is a business expense for you, right?

Lillian Karabaic: So that the same as we’ve talked about like when I pay will as my my business Oh My Dollar!, Like I’m not paying personal taxes on the amount of money, right?

Lillian Karabaic: OK. So yeah generally it is it is a thing that you can get a payroll deduction. Obviously, if you’re at the point where you have eight employees for your business, I hope that you are working with a qualified tax professional. If you’re not one yourself and simply because there is a lot of things to consider around this and you want to make sure you don’t miss any of those local taxes and things like that.

Lillian Karabaic: OK. So 401K hopefully have maybe scared you away from that a little bit unless you’re really up for a challenge maybe, you are you listen Oh my dollar! The other options you can do are quite simply helping your employees, if you’re a small employer you’re not planning to massively grow, One of the options you can do is just encourage your employees to set up a IRA.

Lillian Karabaic: There is an incredibly easy program set up by the government called myRA..

Will Romey: Oh cute.

Lillian Karabaic: Yeah. They try. They try.

Will Romey: That’s a good pun for the government.

Lillian Karabaic: I know for the government they’re trying. And the myRA is pretty nice because there’s no cost to employers to set up. You don’t need to administer employee accounts, and you don’t need to match or contribute to employee contributions. The government provides all the materials you just set up and be above the law with this. And essentially those accounts are Roth IRAs for your individual employees. So it’s very good if you’re like, for example like you own a coffee shop and you have a lot of kind of lower-income employees that might be younger, to make sweeping generalizations about coffee shop employees that are probably correct, if you’re in that case you probably have a lot of employees that maybe don’t have any kind of IRA set up and the MyRA is meant to be kind of a starter IRA.

Lillian Karabaic: The downside of this, in my opinion, is that these accounts are 1) they’re made with after tax dollars so for some people that might not make sense. Roth – We know the difference between Roth versus Traditional – but also they are locked up into savings bonds.

Lillian Karabaic: So rather than, as we encourage you want to invest for long term growth, on this and we want you to be invested in you know things that are going to give you a higher rate of return over the long term.

Lillian Karabaic: Bonds are when you’re younger should be a very small part of your overall portfolio. What the MyRA is – is it tries to ease you in by giving you a guaranteed rate of return which is equal to the G Fund of the government’s Thrift Savings Plan fund. They’re essentially government bonds. And right now they give 1.875% right.

Will Romey: Which is not. I mean that’s still better than most bank accounts.

Lillian Karabaic: Better than a checking account.

Lillian Karabaic: It’s good if you’re scared of getting started. The other thing about this is it is very, very, very much meant to be a starter plan. So once you get to $15,00 in that myRA per employee they have to roll it over into a privately held Roth IRA.

Will Romey: It’s almost as sort of encouraging them to kind of get over there.

Lillian Karabaic: Just get started.

Lillian Karabaic: And we’ve talked before. Oregon is implementing this thing called Oregonsaves. And Oregon saves is pretty much similar to myRA, except it is not necessarily locked up into a G Fund. It’s locked up into target retirement funds based on when the employee is going to be hitting retirement age.

Will Romey: So then some some sort of combination of bonds –

Will Romey: and bonds.

Lillian Karabaic: Bonds and stocks.

Will Romey: Bonds and stock.

Lillian Karabaic: Yeah yeah yeah definitely. So the myRA is a good option. If you’re just trying to get your toe in the water for those – they aren’t necessarily going to be the best option, but they are essentially set up for this, which is please offer something and please encourage your employees to get their toe in the water.

Lillian Karabaic: Another option in kind of that vein is just set up a Roth or Traditional IRA – that you can either administer these, you can help your employees set them up, but they are technically their own accounts. So the downside of this is that you won’t be able to match. So if you want to give any kind of employer contribution, the only thing you can do is help your employees save pre-tax money out of their paycheck, and put it into their own account.

Will Romey: Right. So having that kind of automatic deduction.

Lillian Karabaic: Yeah. And those automatic deductions, technically you can set up for any employee if they have their own IRA they, already set up outside of work. But obviously you’re a small employer, and probably most employees don’t know that. We’ve talked about it before on the show but a lot of people don’t automatically know that that’s a thing they can ask their employer to do.

Will Romey: A majority of employees worldwide don’t yet listen to Oh My Dollar!

Lillian Karabaic: Yes we’re working on it but now. Yeah but not yet.

Lillian Karabaic: So that is another option if you just want to like encourage your employees, one thing, you can do is just set aside an employee learning day – you know give them donuts and say “hey I want to encourage you as as employees to set up IRAs.”.

Lillian Karabaic: And here is the form in which I will, I will help, you know, help you take this automatically out of your paycheck and get saving. The downside is you can’t offer that then that cool carrot which is employer contributions.

Will Romey: That Matching

Lillian Karabaic: That Match. All right. We are going to take a quick break. Reminder that oh my dollar is supported by listeners like you through our patron and by sponsors. We’re gonna come back and talk about the other options for setting up employer retirement plans. But first we’re going to take a quick break to hear from our sponsors.

Will Romey: Yes BRB.

Will Romey: So Will, if you were an employer with eight employees, You know your easy options. Yeah. MyRA and you know just helping your employees with whatever their IRA is.

Lillian Karabaic: Almost all of these options don’t have matches that we’ve talked about.

Lillian Karabaic: So they don’t have matches.

Lillian Karabaic: And the other downside is you as an employer might be making some money, you’re a business owner maybe you want to reduce your taxable income not a lot you can do with these right like these have pretty low limits.

Lillian Karabaic: So the IRA limits are six thousand a year. And you know that isn’t that doesn’t reduce your taxable income that much. So what are your other options?

Lillian Karabaic: Well if you want to go the complete opposite of not being able to give an employer contribution there is also these SEP IRA which is a simplified employee pension.

Will Romey: That sounds simple and matching.

Lillian Karabaic: It sounds simple it’s really not that simple but it is very much a matching because it is only employer contributions.

Will Romey: So an employee pension. That makes sense.

Lillian Karabaic: Yeah yeah. If you remember those good old days, where people had pensions through their jobs.

Will Romey: I do not. Heard of it.

Lillian Karabaic: I’ve heard about them in shows and the news occasionally.

Lillian Karabaic: These are for self-employed people, or small business owners and a small business owner with one employee or more or anyone with freelance income can open a simplified employee pension. They can be really good retirement option for small business or sell or self-employed people as they’re relatively easy to setup and individuals don’t have to pay taxes on the dividends or capital gains that the investments earn = which is you know a big deal it helps long term in saving for retirement.

Lillian Karabaic: The easy way that you set them up is that you essentially make sure that you get the correct forms from the institution that administers them.

Lillian Karabaic: And then you need to make sure that you deposit SEP contributions in to each of your employees accounts. And there’s quite a lot that you can put into these SEP IRAs. These Sep IRAs are only employer contributions, though – so see you.

Will Romey: So we feel so for the goal of helping your employees save for retirement, You’d also want to encourage them to set up their own Roth.

Lillian Karabaic: And and what is very helpful is if you’re a sole proprietor you don’t have to really worry about that, right?

Lillian Karabaic: But you get to set up who qualifies for the plan. But there’s upper limits on who you can deny access to the plan. So, it’s good to know essentially like if you have an employee I think I think the maximum limit is if you have an employee that’s worked for you for three out of five years you, you have to be contributing to their SEP IRA. And what level you set has to be across the board the same. So.

Will Romey: Right. So they’re just insuring your group being consistent – fair across all your employees. So you’re not just like screwing Jack from down the hall.

Lillian Karabaic: Yeah exactly. Well and the big thing is that they don’t want you as an owner to be like I want to give myself 100 percent of my income, but then I’m not going to contribute for anyone else. If you want to do that there’s other options right?

Lillian Karabaic: So contributions are only made by the employer but you can go up to a maximum of fifty six thousand dollars a year.

Will Romey: That is nice max. Yeah.

Lillian Karabaic: It’s a good Max. Of course it is based on your total gross amount of money that your business is making. You know this is a pre-tax contribution just the same as it would be for traditional 401K or a traditional IRA, which means that they’re taxed at withdrawal, but it means you lowers your taxable income.

Will Romey: Yup. I follow.

Lillian Karabaic: It’s pretty cool. So the way that you set these up is that you need to find it administer for the program if you want to do a SEP IRA.

Will Romey: That’s got to be a third party like you can’t administer your own?

Lillian Karabaic: You can’t administer. You do have to hold the paperwork and you will you know need to set up whatever automatic transfers you’re doing in order to deposit in the account. But yes, you need a brokerage. So unless you’re a small business of eight people which happens to be an investing brokerage, which is pretty much doesn’t exist then, yes you do need to set up with a third party and you know you can kind of just stumble around and look for a SEP IRA – some of the typical ones that small businesses use are Fidelity, Vanguard, and you can you can look around. One of the biggest recommendations I have here is to ask other small business owners,.

Will Romey: what’s working for them, what they’ve tried.

Lillian Karabaic: Yeah. What they like. What doesn’t make them angry to deal with.

So now, what if you’re in between – you’re like you don’t want to not match anything, you don’t want to deal with the heavy administration of the 401K, but you want to be able to contribute a little bit and encourage your employees to save for retirement? Well one of the other options for you is something called a Simple IRA.

Will Romey: Is it?

Lillian Karabaic: Not a simplified employee pension but a simple IRA. And I will say, it is actually simple it is actually also an acronym because it’s the government.

Will Romey: What does it stand for? I got to know.

Lillian Karabaic: Oh my God I don’t know, I don’t know. I don’t knooow!

Sorry. Can’t something is an acronym and not follow up.

Lillian Karabaic: It stands for Savings Incentive Match Plan for an Employee’s Individual Retirement Account.

Will Romey: Sounds like simpflee.

Lillian Karabaic: They tried.

Will Romey: Simpflea IRA

Lillian Karabaic: Like many government things it is a acronym and it is cool because I think it’s one of the best options for a small business owner because it allows you to sidestep a ton of that heavy lifting that you need for other sponsored retirement plans, like a 401K, which have all of those hefty reporting and administrative duties.

Lillian Karabaic: They’re more simple than a 401K – quite, quite simply the name the advertising in the name is true.

Lillian Karabaic: But the cool part is they allow employees to contribute for themself, unlike the SEP IRA – there there’s also no IRS filing requirements for the employer.

Lillian Karabaic: But the thing about this, is if you have a simple IRA you can’t have another retirement plan in place.

Will Romey: Like for the business or?

Lillian Karabaic: For The business. Yeah. So you can’t have like a SEP IRA and a SIMPLE IRA or a 401K and a SIMPLE IRA – that because by doing that you’d sort of –

Will Romey: You could exceed the limits on either or both.

Lillian Karabaic: Yes definitely. But you could also have a IRA setup on your own. Even though they have IRA in the name you can have your own individual retirement account as an owner or an employee and a simple IRA.

Lillian Karabaic: And those limits do not count against each other.

Will Romey: Okay.

Lillian Karabaic: So that is good to know because we do know that traditional and Roth IRAs count as part of the same six thousand dollar a year limit.

Will Romey: Yeah.

Lillian Karabaic: Just to make it confusing these all have IRA at the end even though they’re all totally different kinds of accounts.

Will Romey: Simple – SIMPFULL!

Lillian Karabaic: Simple IRA is really really fascinating. And I do think it has in many ways some of the best administration. And it is one that you can also do as a non-profit, if for if you know you’re too small of a non-profit to really do a 401K or a 403B, SIMPLE IRA can be a good option. The thing here, though, is that the employer has to match the employee contribution on a dollar for dollar basis up to 3 percent of the employee’s salary.

Lillian Karabaic: Or they have to make what’s called a non-elective contribution, which means that even if the employee doesn’t choose to save the employer has to make a contribution instead of the matching.

Will Romey: I don’t think I understand that.

Lillian Karabaic: Essentially you have to put in money for each employee regardless of whether or not they save in the SIMPLE IRA

Will Romey: or you match.

Lillian Karabaic: Yep. Okay. Okay that makes sense. I think that’s the IRA. Very briefly had at a place before I left, because I remember the 3 percent – up to 3 percent specifically or is that consistent across other IRAS?

Lillian Karabaic: It’s a very common amount for 401K matching, but the simple IRA is kind of nice because the employee keeps the account. It’s in it’s their own account. It’s not something administered by your, your employer so you don’t have to deal with that rollover problem that you have to deal with if you leave your employer.

Will Romey: Oh that’s nice.

Lillian Karabaic: And as an employer it’s it’s I think one of the easiest ones to administer. Short of just not having one, right?

Will Romey: Easiest to administer.

Lillian Karabaic: And it’s one of the only ones that makes it fairly easy to contribute. You can set your own requirements, for who qualifies for the plan but just like the SEP IRA there is an IRS limit where you can’t, you know just choose to exclude people so any employee earning at least five thousand dollars during any two years before the current calendar year, and who expects to make at least that in the current calendar year has to be able to participate in the plan.

Lillian Karabaic: Which means that if you’re doing the automatic contributions, you’re gonna have to give 2 percent into everyone’s plan as the employer, regardless of whether or not they’re saving or whether or not you like them, Right?

Will Romey: Okay I follow.

Lillian Karabaic: Does that make sense?

Will Romey: Yes!

Lillian Karabaic: The other thing to know is that you’re you are able to adjust the amount that you are contributing as an employer to the plan up or down between like 3 or 2 or 1 percent year-to-year.

Will Romey: You’re not tied to that.

Lillian Karabaic: You’re not entitled to that, but it is kind of a pain in the butt and there is a limit to how much you can adjust it, and you can’t adjust it down to zero for more than like one year out of every five.

Will Romey: So because then you just don’t have it.

Lillian Karabaic: Yeah. Then you just don’t then it’s just not matching. And so what’s important to kind of know about that is that you are kind of locking yourself into giving everybody a 2 percent raise if you do this. But if you’re, if you’re committed to doing that IRA, that 2 percent raise if you don’t have a lot of employees can can end up being less than the administration fees for something like a 401K –

Will Romey: Staff member to run that or your own time and running that.

Lillian Karabaic: Yeah exactly. And you’re contributing to your employees retirement.

Will Romey: Which is our stated goal here too.

Lillian Karabaic: Yeah. Yeah. And also.

Will Romey: Mission accomplished.

Lillian Karabaic: And helping them save it. And it’s a good carrot right? Like it’s a good carrot for your employees. If you do, if you structure it as a match.

Lillian Karabaic: So those are pretty much your options as a small business and small business that wants to set up retirement. There is also profit-sharing but we aren’t going to do a ton of emphasis on that. But it can be a good incentive for a small for-profit employer that wants to figure out a way to encourage their employees to both help with making the business be better, and also helping helping them save for retirement.

Lillian Karabaic: Those the profit-sharing is more complicated to set up, but you usually set it up the same as you would do a payroll deduction.

Lillian Karabaic: And quite often you can do this so that it is set up within one of these different workplace retirement plans.

So if you do want to do profit-sharing you could do it in something like a SEP or a SIMPLE IRA and profit sharing just allows you to you know structure some kind of work incentive in with retirement saving which can be a good option, if you are a small business right?

Will Romey: Another carrot like you are saying.

Lillian Karabaic: Yes! And a carrot to do more work not just general.

Will Romey: Not just a snack.

Lillian Karabaic: So those are your options. Setting up a 401k – it can can be costly and a bit of an administrative headache. Simple IRA is a good option, but you will have to contribute for your employees. A SEP IRA, you will also have to contribute for your employees but the great news is that it can be a really good way to lower your taxable income as an owner and your Roth or Roth, Traditional or MyRA., done through employer deductions. Those are good options if you aren’t able to do a match, but you just want to encourage your employees to start saving for retirement.

Will Romey: That’s perfect. Yeah. There’s a lot of good options. A couple mediocre options

Lillian Karabaic: Yeah I mean they’re kind of across the board. If you are at a small employer in Oregon, you’re being phased into the- That doesn’t currently have a retirement plan for employees – If you are an Oregon employer listening to this and you are a small employer that does not yet have a retirement plan in place, you will be phased into the Oregon saves program.

Lillian Karabaic: We did an episode about that last year maybe, two years ago? But it’s being slowly phased in over the next couple years so I will link in the show notes about that. It’s essentially the IRA option that we talked about excep it is administered by the state, and so it eliminates some of the headache for you.

Lillian Karabaic: So yeah it has pretty much the same downsides as the IRA options that we talked about on this, but you will be required to either opt-out by saying you have access to another retirement plan for your employees or you will be required to enroll in that. So if you’re an Oregon employer you could just ignore it and this problem will solve itself.

Will Romey: That’s interesting though this is true is sort of being being made mandatory in a way that seems worthwhile.

Lillian Karabaic: Yeah.

Will Romey: As an employee.

Lillian Karabaic: Oregon has one of the lowest rates of retirement savings in the country. And some of the least prepared citizens for retirement.

Will Romey: Sounds Like Oregon.

Lillian Karabaic: So Oregon is working very hard to try to fix that, but they also want to be a leader on this kind of policy at the national level. And so yeah we have a whole interesting episode with one of the folks from that state program. Oregon saves.

Lillian Karabaic: Oh yeah. Okay. Was having trouble placing that episode.

Lillian Karabaic: It Was a long time ago.

Lillian Karabaic: It was a long time ago. Yeah it takes. It turns out it’s a long time to roll out a statewide retirement plan.

Will Romey: So it impacts every employer it ever impacts.

Lillian Karabaic: Every employer including if you are self-employed. But that’s not for a couple of years. But if you’re self-employed, all you have to do is opt out and say you don’t want to do it.

Lillian Karabaic: So I think that is it for today.

Lillian Karabaic: I hope that helped. If you are someone that is has a small business or even is self-employed and just looking for ways to reduce your taxable income.

Will Romey: Awesome.

Lillian Karabaic: Thank you for listening. Reminder. We love hearing from you. Email us your financial worries or successes or questions about IRAs at questions@ohmydollar.com Or tweet us @anomalily or @ohmydollar

Will Romey: Our producers Will Romey, our intro music is by Aaron Parecki and your host and personal finance educators Lillian Karabaic. Thanks for listening. Until next time remember to manage your money, so it doesn’t manage you.

Sparkle sound: SPARKLES.

Lillian Karabaic: WEEE!

Sonix is the best online audio transcription software in 2019.

The above audio transcript of “How to Choose An Employee Retirement Plan as a Small Business” was transcribed by the best audio transcription service called Sonix. If you have to convert audio to text in 2019, then you should try Sonix. Transcribing audio files is painful. Sonix makes it fast, easy, and affordable. I love using Sonix to transcribe my audio files.